People often confuse “a growing market” with “a profitable market”. They are not the same thing: a sector can grow fast and leave margin for no one. Michael Porter’s model, set out in 1979, is built for exactly that, to understand where an industry’s profitability is decided, and who captures it.

The idea fits in one sentence. A sector’s profitability does not depend on direct competition alone, but on five forces that all bear on the margin. The stronger these forces, the less profitable the sector, no matter how good your product is. It’s a diagnostic grid, not a crystal ball: it doesn’t tell you whether you’ll win, it tells you where the value leaks out.

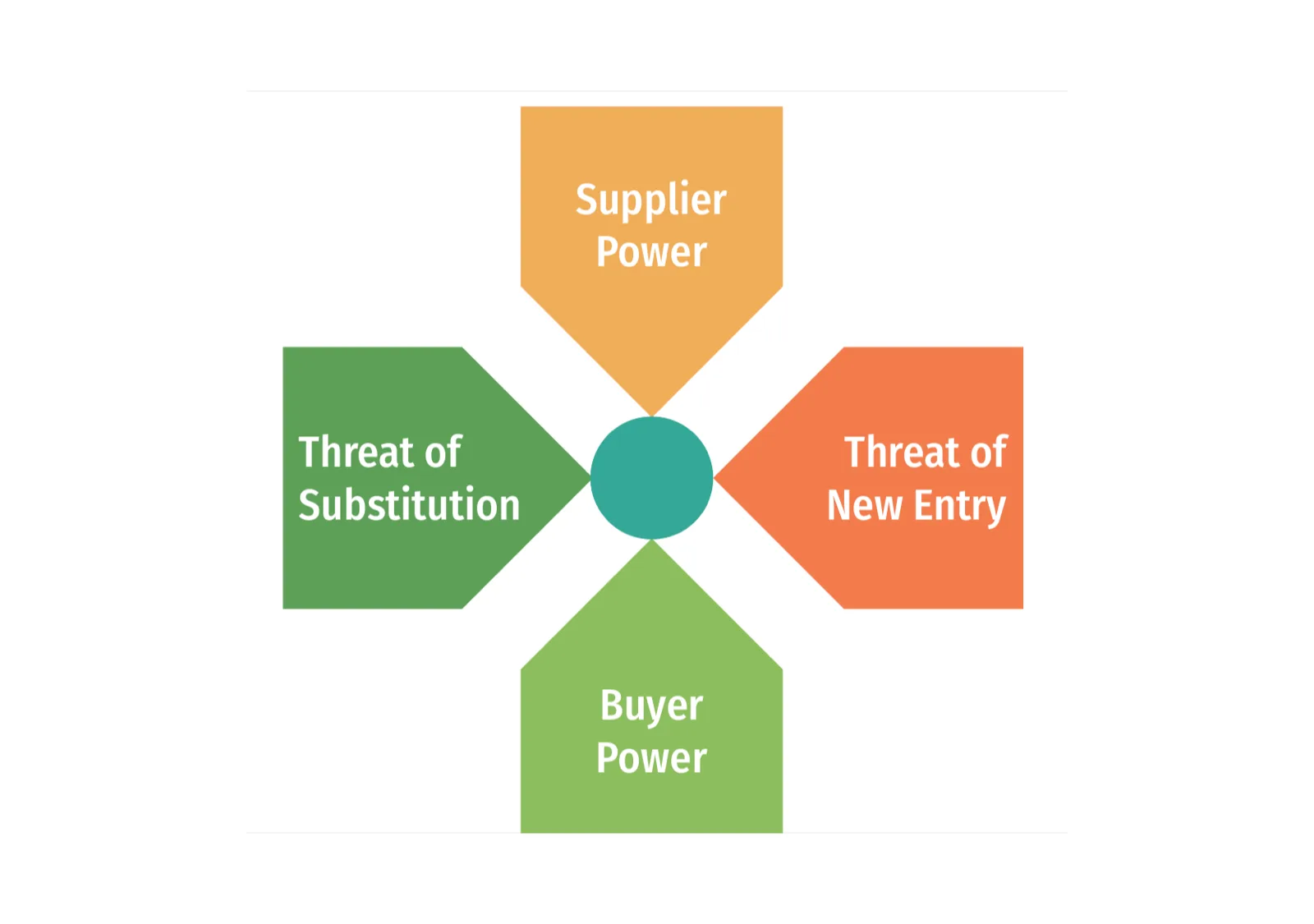

the central force: rivalry among competitors

This is the heart of the model, and the result of the other four. Rivalry is intense when competitors are numerous and of similar size, when the market grows slowly (you only grow by taking share from others), when products look alike, and when fixed costs are high (you have to fill capacity, so you cut prices). Strong exit barriers make everything worse: players who can’t leave keep slashing prices.

In hardware, the market for off-the-shelf boards and modules shows the mechanism well: many players, weak differentiation, easy catalogue comparison. The battle is fought on price, and margin evaporates. Conversely, a certified product that is hard to copy keeps rivalry gentler.

the bargaining power of suppliers

A supplier is powerful when it can impose its prices, lead times or quality on you with no room for you to react. That happens when suppliers are few, when the component has no equivalent, when you are a small volume to them, or when switching supplier is expensive (requalification, recertification).

This is a daily reality in electronics. A single-source component (a specific MCU or FPGA) dictates its terms, and the 2021-2022 semiconductor shortage showed what happens when the force swings entirely to the supplier’s side: allocations, multiplied prices, 52-week lead times. The defence is structural, plan for a second source from the design stage, and design for availability rather than for raw performance.

the bargaining power of buyers

The mirror image of the previous force. A buyer is powerful when it can drag your prices down or demand more service. That happens when buyers are concentrated, when one of them accounts for a large share of your revenue, when your product is undifferentiated (the buyer compares and plays competitors against each other), or when it can simply make in-house what you sell it.

For a subcontractor, the classic danger is the key account that represents half the order book: it sets prices because losing it would be fatal. The defence runs through differentiation (a skill not found elsewhere) and through spreading customer risk.

the threat of new entrants

The question isn’t only “who are my competitors today”, but “how easy is it for new ones to appear”. What protects a sector are the barriers to entry: capital required, economies of scale, access to distribution, patents, brand, and above all, in hardware, certification.

This is a strength of regulated electronics. The cost and time of a CE, EMC, medical or railway certification are a real barrier: you don’t enter these markets in a quarter. That barrier protects incumbents. Conversely, a consumer connected product with no regulatory constraint is exposed to a competitor landing within a few months.

the threat of substitutes

Not to be confused with new entrants. An entrant offers the same product as you; a substitute meets the same need with a different solution. It’s often the most insidious threat, because it comes from outside your sector.

Examples abound in electronics: a dedicated sensor replaced by a function already in a smartphone, a wired function replaced by software, a physical box replaced by a cloud service. A substitute becomes dangerous as soon as it offers a better price/performance ratio and switching costs are low. You watch for it by looking at the customer’s need, not just at your direct competitors.

how to use it

The model has two concrete uses. Before entering a market, it helps you judge whether it’s attractive: five weak forces signal a profitable sector, five strong ones signal a permanent brawl. On an existing activity, it helps you locate the margin leak and choose a response: differentiation to ease rivalry, a second source to reduce supplier power, certification or patents to raise the entry barrier.

Keep its limits in mind. It’s a snapshot at a given moment, not a dynamic: it doesn’t capture technological disruption well. It ignores complementors (what some call the sixth force), the players who make your product more useful without being either customers or suppliers. And it was designed for established industries, less so for a fast-moving software ecosystem.

what to remember

The Five Forces don’t predict the winner, they show where the margin is decided and who captures it. A good product in a sector where all five forces are strong will stay barely profitable; an average product in a protected sector can do just fine. Before asking “how do I win”, the right question is “does this sector let anyone win”, and the answer is read in these five boxes.

Diagram adapted from a Slidesgo infographic template (original text removed, content rewritten). Visual credit: Slidesgo.